Deep|Global IT Budgets Under Pressure: Macro Uncertainty, AI Momentum, and the Rise of Digital Sovereignty

Interviews with 10 Channels and Customers

On April 2, President Trump officially declared “Liberation Day,” triggering a renewed wave of tariffs and escalating trade tensions. While software and IT services may not be directly subject to tariffs, they are deeply intertwined with the broader economy. In an environment where the real economy faces rising pressure and volatility, we believe it’s critical to examine how software spending patterns may evolve in response.

Due to the short turnaround time, our primary research was somewhat limited. To compensate, we’ve supplemented our findings with a broad review of recent sell-side reports and channel checks, aiming to piece together a comprehensive view of the current landscape and the early signals emerging from enterprise IT buyers.

We believe this report is very important ahead of the upcoming SaaS earnings season.

The content of this report is very solid, covering various IT budget areas. Additionally, through our interviews, we uncovered several previously unmentioned phenomena such as increasing headlines on European companies looking for domestic vendors to replace US counterparties.

"Some 30% of European customers are considering switching to local vendors such as SAP, at least for their European operations," said the Global Partner.

Evolving IT Spending Estimations

(1) Budget revisions underway amid macroeconomic uncertainty

Client-side sentiment is shifting downward, per recent sell-side surveys and channel checks. Many enterprises are now preparing to revise their 2025 IT budgets down.

The first half of 2025 is relatively insulated, as most plans were locked in during Q2/Q4 last year. Cuts have largely focused on trimming within pre-approved envelopes

The second half is more exposed, especially among companies on new fiscal years or those conducting mid-year reviews. If macro conditions deteriorate further, we could see flat or reduced budgets in H2.

(2) Recent sell-side commentary:

KeyBanc: 61% of respondents observed worsening macro trends in the past 90 days; 6% flagged “significant deterioration,” most post-April 4, likely tied to tariff concerns (dubbed “Liberation Day”).

Citi: Over 50% of CIOs expect tariffs to drive budget reductions in the next 12 months. The Q1 IT budget growth outlook saw its first downward revision in six quarters.

UBS: Two leading SaaS partners reported anticipated budget freezes and cuts by clients who had previously planned to restart spending in 2H25. Cuts may not be as drastic as 2022, as SaaS budgets have already been optimized in prior years. (During the 2022-2023-2024 cycle, there was a significant spike in consumer spending, largely driven by the pandemic. People were over-purchasing goods and services, which led to a surge in demand. By the second half of last year, it seemed like we were emerging from that period. The consensus was that we'd be on the path to recovery in 2025, and budgets were starting to ease up a bit. However, just as we were beginning to see signs of a rebound, we hit this current snag. It's pushed us back to the previous pace, and unfortunately, there wasn't much of a buffer left for further downgrades. As a result, the adjustments we're making aren't too drastic.)

Morgan Stanley (MS): CIO sentiment shifted notably between early and late February, from a 1.3x upgrade/downgrade ratio to just 0.5x—the weakest since Q3 2023.

Wolfe Research: SMB-focused channels remain more bullish than enterprise-focused ones, but enterprises are increasingly cautious amid policy uncertainty.

(3) Channel checks – direct feedback:

US Channel Partner: “~20% of clients have cut or are planning to cut. We estimate 40% may reduce spending for the year, averaging a 5-8% cut.”

European Channel Partner: “30% of clients are planning to cut budgets this month, mostly by 3–5%. Some are already cutting due to layoffs reducing seat counts.”

North America CRM Partner: “Roughly 20–30% of customers are considering phased reductions.”

North America CSP: “Our IT budget growth outlook has been revised down from 11–15% to 9–12%.”

North American Beverage Brand: “Our industry was already weak; trade tensions will hit harder. FY25 IT budget was planned to grow 2–3%, but in reality it’ll be flat. FY26 will also likely be 0%.”

(4) Gartner waarning – april 8 update:

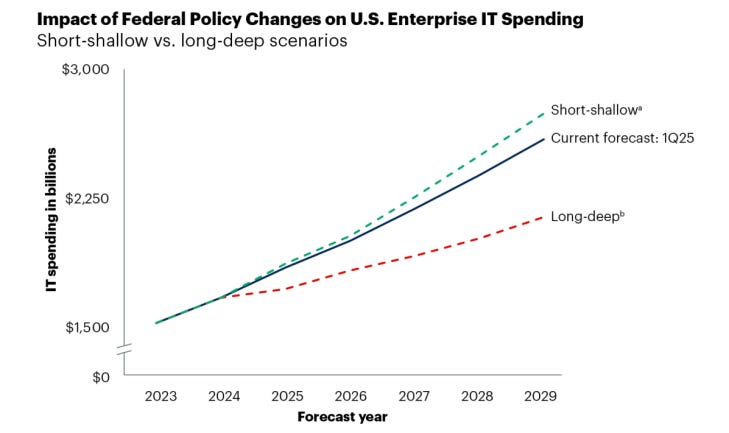

Two scenarios were outlined: Short-Shallow (Optimistic, the green line): A brief trade conflict ends by summer 2025; the U.S. economy recovers by 2026, with modest federal cost cuts and pro-investment policies. IT spending grows from 10.5% to 11.9%.; Long-Deep (Pessimistic, the red line): A prolonged trade war through 2029 slows growth dramatically, prompting deep government spending cuts and eroding business/consumer confidence. IT budget growth falls to just 3.2% in 2025.

Sector-Level Impact:

A. Sector with High Negative Impact:CRM and IT Services Hit Hardest, Workflow and ERP Show More Resilience

(1)CRM (e.g., Salesforce, Microsoft, HubSpot, Zoho): the most exposed category in this cycle.

Among revenue-generating tools, CRM solutions are the quintessential example—think Salesforce. Why does this category take the hardest hit? When the industry is in a downturn, boosting revenue is an uphill battle. Most companies' go-to strategies are to downsize and streamline costs. This means that the marginal benefit of investing in these software solutions plummets, making them the first to get the axe.

North American CRM Expert: “CRM platforms like Salesforce are heavily impacted. Seat-based pricing models are directly affected by customer layoffs—some clients are cutting up to 30%, while struggling businesses are slashing licenses by 70% or more. Others are reducing seat count during renewal or switching to cheaper SKUs.”

Channel Partner: “CRM is inherently tied to revenue expansion. In a downturn, these platforms perform worse than cost-control tools.”

Smaller Channel Partner: “We originally expected 20% growth in CRM sales this year. Now we’re targeting a 5% contraction. Companies deprioritize tools that enhance customer engagement in a weak economy.”

Top-tier IT Consulting Firm: “CRM is being trimmed, though not as essential as ERP—so it's easier to cut.”

(2) Workflow Software (e.g., Workday, ServiceNow, Monday.com): less impacted than CRM, but still seeing pressure.

Keep reading with a 7-day free trial

Subscribe to FundamentalBottom to keep reading this post and get 7 days of free access to the full post archives.